free shipping at $99

When you hear "cash flow management," it really just means keeping a close eye on the money moving in and out of your business. It’s not about how much profit you’re making on paper; it's about making sure you have actual cash in your bank account to cover bills, pay your team, and grab growth opportunities when they pop up. Think of it as the financial heartbeat of your company.

This is a tough lesson many entrepreneurs learn the hard way: you can be wildly profitable but still have no money in the bank. It's a dangerous gap, and it's where countless promising businesses trip up and fall. Profit is a number on a spreadsheet, an accounting concept. Cash is the real-world fuel you need to operate day-to-day.

Let me give you a classic example. Imagine a local bakery that's absolutely crushing it. Their cakes are the talk of the town, sales are through the roof, and their profit and loss statement looks amazing. But behind the scenes, the owner is sweating bullets trying to pay her flour and sugar suppliers. How is that even possible?

A huge chunk of her business comes from big corporate catering orders. She delivers a mountain of beautiful pastries, sends an invoice, and slaps "Net 30" payment terms on it. She's technically earned that money, but the cash itself won't land in her account for a whole month. In the meantime, rent is due, her bakers need to be paid, and she has to buy more ingredients for next week's orders.

The bakery is profitable, but it isn't cash-flow positive. Grasping this distinction is probably the single most important thing you can do for the financial health of your small business.

This isn't just some business school theory; the consequences are very real and very severe. It’s a shocking number, but 82% of small businesses that fail do so because of poor cash flow management.

Even more sobering? A full 29% just plain run out of cash, forcing them to lock the doors for good. These figures from small business cash flow statistics on llcbuddy.com prove that getting a handle on the movement of money is often more critical for survival than just making sales.

Once you really understand this core difference, everything else starts to click into place. The goal is to build a business where your cash coming in consistently stays ahead of your cash going out. That’s what gives you the stability and the freedom to stop stressing and start growing with confidence.

A cash flow forecast isn't just another accounting chore to check off your list; it’s the financial roadmap that guides your business decisions. Think of it as a weather forecast for your finances—it helps you prepare for sunny growth periods and navigate potential storms, ensuring you're never caught off guard.

The good news? You don’t need an accounting degree to build one. It just takes a realistic look at your money coming in and your money going out.

The first piece of the puzzle is figuring out how much cash you actually expect to come in. This is more than just wishful thinking; it’s about using real data to make an educated guess.

Start by looking at your sales from the same period last year. Did you have a seasonal rush? A predictably slow month? Digging into these patterns is the best way to anticipate the natural peaks and valleys in your income.

From there, factor in your current sales pipeline. If you’ve just landed a big project or have several promising leads that are likely to close soon, you can build those expected payments right into your forecast. This gives you a much clearer picture of the cash you can realistically expect in the coming weeks and months.

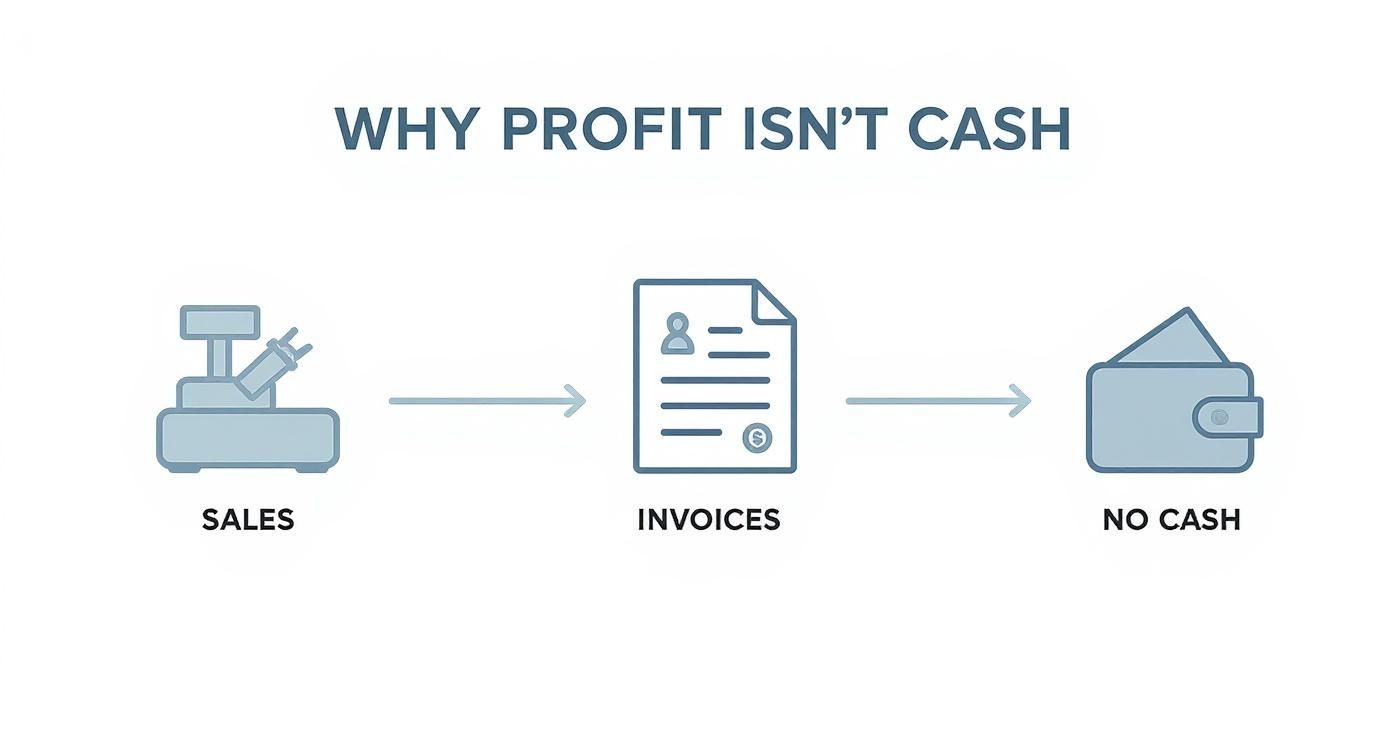

This infographic really drives home the crucial gap between making a sale and having cash in hand.

As you can see, profit on paper doesn't immediately become usable cash—a classic challenge every small business owner has to manage.

Once you have a handle on your expected income, it's time to map out your expenses. I always recommend starting with the easy stuff: your fixed costs. These are the bills that stay the same every single month, no matter what.

After you've listed your fixed costs, it's time to tackle your variable expenses. These are the costs that go up and down based on your business activity. For anyone running a product-based business, a great example can be found when learning how to start a candle-making business, where the cost of wax and fragrance oils scales directly with how many candles you produce.

Other common examples include things like marketing spend, shipping fees, or payments to hourly contractors.

A truly realistic forecast doesn't just list expenses—it anticipates them. If you know a big annual insurance premium is due in three months, put it in the forecast now. That way, you can start setting cash aside and won't get hit with a nasty surprise.

To make this feel more real, let’s look at how this plays out for a freelance graphic designer.

By reviewing her past year, she knows that business always slows down in the first quarter right after the holiday rush. So, when building her forecast, she projects lower income for January, February, and March based on this historical trend.

Seeing this projected dip gives her a heads-up. She decides to delay a non-essential equipment upgrade and pulls back her marketing ad spend for those three months. Because her forecast gave her an early warning, she can navigate the slow quarter without any stress. Her cash balance stays healthy, and she's ready for when business picks back up in the spring.

This simple act of forecasting transforms her from reacting to financial surprises to strategically planning for them.

Here's a simplified look at what a basic cash flow forecast might look like for a small retail shop.

| Category | Projected Amount | Actual Amount | Difference |

|---|---|---|---|

| Cash Inflows | |||

| Sales Revenue | $15,000 | $16,200 | +$1,200 |

| Loan Disbursement | $0 | $0 | $0 |

| Total Inflows | $15,000 | $16,200 | +$1,200 |

| Cash Outflows | |||

| Rent | $2,500 | $2,500 | $0 |

| Inventory | $6,000 | $6,500 | -$500 |

| Payroll | $4,000 | $4,000 | $0 |

| Utilities | $500 | $450 | +$50 |

| Marketing | $1,000 | $1,200 | -$200 |

| Total Outflows | $14,000 | $14,650 | -$650 |

| Net Cash Flow | $1,000 | $1,550 | +$550 |

By tracking projected vs. actual numbers like this, the retailer can quickly see where they over- or underestimated, making their next forecast even more accurate.

Let’s be honest—waiting for money to land in your account can be one of the most agonizing parts of running a small business. Getting cash in the door faster isn't just about sending out invoices and hoping for the best. It’s about being strategic and actively encouraging clients to pay you sooner.

The whole game is about shortening the time between when you deliver your work and when that cash is actually usable in your bank account. This is often called shortening the cash conversion cycle, and it’s one of the most powerful moves you can make to get a handle on your cash flow.

One of the most direct ways to get paid faster is to take a hard look at your payment terms. If you've been using "Net 30" just because it's what you've always done, it's time to ask if it's really serving your business's health.

Making the switch to Net 15 can be a game-changer, instantly cutting your potential wait time in half. Sure, some big corporate clients might have rigid payment cycles, but you'd be surprised how many are perfectly fine with shorter terms if you set that expectation from the start.

Here's another trick I've seen work wonders: offer a small discount for paying early. A "2/10, Net 30" term, which gives clients a 2% discount if they pay within 10 days, is a fantastic incentive. For a client with a $5,000 invoice, that $100 savings is often all it takes to get your invoice moved to the very top of their to-do list.

Don't just send an invoice and hope for the best. Proactively guide your clients toward faster payment through clear, beneficial terms. It frames the relationship as a professional partnership where timely payments are expected and appreciated.

The harder it is for a customer to pay you, the longer they're going to take. Seriously. If your only payment option is mailing a physical check, you are actively slowing down your own cash flow in an age of instant transactions.

To speed things up, give them multiple, super-convenient ways to pay:

Making it easy to pay is also a massive part of improving ecommerce conversion rates. A clunky checkout leads to abandoned carts and lost sales. The exact same idea applies to your service-based invoicing.

Nobody enjoys chasing down late payments. It's awkward, uncomfortable, and a total time-suck. This is where a polite but firm automated follow-up system becomes your best friend.

I once worked with a small consulting firm that was struggling with an average collection time of 48 days. They set up simple automated emails—a friendly heads-up a few days before the due date, one on the day it's due, and a firmer (but still professional) notice seven days after. That single change cut their average collection time down to just 24 days. It was a massive win for their cash position, and it didn't burn a single bridge with their clients.

Of course, there will be times when your inflows just aren't enough to cover a big growth opportunity. In those moments, knowing how to get a small business loan can give you the capital you need to bridge the gap. Think of it as a temporary boost while you work on getting your receivables system dialed in. A combination of smart invoicing, easy payment options, and consistent follow-up is what truly creates a system that keeps cash flowing predictably.

Managing your cash flow isn't just about getting paid faster; it’s about being incredibly smart with every dollar that leaves your bank account. I'm not talking about blindly slashing costs in a way that stunts your growth. This is about taking a strategic look at your spending and making sure every single dollar is pulling its weight.

The real goal is to get intentional. You want to analyze where your money is going, find efficiencies, delay payments where you can, and cut the fluff. This approach keeps more cash on hand, giving you a much stronger financial cushion and a lot more breathing room.

One of the most powerful moves you can make is to simply ask for better payment terms from your key suppliers. If you’ve been a good customer and have a solid payment history, you have way more leverage than you probably think. Sometimes, a single conversation can make a world of difference.

Are you always accepting the standard "Net 30" terms? Try asking if they'd be open to Net 45 or even Net 60. Just like that, you’ve given yourself an extra 15 to 30 days to hold onto your cash. For a business that places regular inventory orders, that simple change can free up thousands in working capital by better aligning your payables with your receivables.

A supplier relationship is a two-way street. Most vendors are willing to be flexible to keep a reliable, long-term customer happy. All it takes is a professional ask where you explain how it helps you manage your business more smoothly.

In our world of SaaS (Software as a Service), those small, recurring charges have a sneaky way of adding up. A "subscription audit" is my favorite quick-win for plugging these silent leaks in your cash flow.

Pull up your bank and credit card statements from the last three months and list every single recurring payment. Then, for each one, ask yourself these tough questions:

I once worked with an e-commerce store that saved over $400 a month just by auditing their Shopify app subscriptions. They found three different apps with overlapping features and two others they hadn't logged into in over a year. That’s nearly $5,000 back in their pocket annually.

Finally, you have to learn the difference between a growth investment and a cash drain. Not all spending is created equal. Sure, cutting your marketing budget to zero saves cash this month, but it could absolutely cripple your sales pipeline for the next quarter.

A growth investment is an expense with a clear, direct line to generating more revenue. Think of a targeted ad campaign, new equipment that boosts your production efficiency, or software that automates your sales follow-ups.

A cash drain, on the other hand, is an expense that doesn't really contribute to growth. This could be that oversized office space, premium software with features you don’t need, or services that just aren't delivering a return.

For example, I advised an e-commerce store that was spending a fortune on premium shipping services. By renegotiating their carrier contracts and offering a slower, cheaper shipping option as the default, they immediately improved their margins without hurting sales. They turned a major cash drain into a manageable, predictable cost.

Trying to run your business finances on manual spreadsheets today is like trying to navigate a new city without a map. Sure, you might get there eventually, but it's going to be slow, stressful, and you’re almost guaranteed to make a wrong turn. For small businesses, simple and affordable technology has become an absolute game-changer for managing cash flow.

These tools aren't just a luxury for big corporations anymore. They deliver the clarity and efficiency you need to turn cash flow management from a reactive chore into a strategic advantage, giving you a real-time snapshot of your company’s financial health.

One of the quickest wins you'll get from tech is automating your invoicing process. Modern accounting software can spit out professional invoices in moments, but the real magic is in the automated follow-ups.

Instead of you having to make those awkward "just checking in on this invoice" calls, the software sends polite, scheduled reminders on your behalf. This simple step not only frees up your time but also helps keep client relationships positive by making the collections process systematic and professional. Plus, it dramatically cuts down on human error.

This digital shift is crucial for healthier cash flow. In fact, just automating accounts payable has been shown to reduce invoicing errors by a whopping 58.7% for businesses that adopt the technology. For a deeper dive, check out the insights on small business cash flow management from caflou.com.

Making it dead simple for customers to pay you is a fundamental rule of good cash flow. This is where digital payment platforms are non-negotiable. By building options like credit card payments or bank transfers right into your invoices, you eliminate friction and shrink the time it takes for that money to land in your account.

Think about it from your customer's shoes. It’s way easier to click a "Pay Now" button than to dig out a checkbook, write a check, and get it in the mail. Faster payments mean faster access to your cash. It's that simple.

Technology closes the gap between when a customer decides to pay and when you can actually use that money. Every single day you can shave off that timeline strengthens your cash position.

Maybe the most powerful tool in your new arsenal is the modern financial dashboard, which is often the centerpiece of good accounting software. This isn't just a static report; it’s a living, breathing overview of your business's financial heartbeat.

At a quick glance, you can see everything that matters:

This kind of real-time visibility lets you make proactive, data-driven decisions instead of just guessing. It helps you spot a potential cash crunch weeks in advance, giving you plenty of time to react. Better financial visibility can also shine a light on your most valuable repeat customers, which is a key piece of the puzzle when you're working on how to increase customer lifetime value.

Even with a solid plan, questions about the nitty-gritty of cash flow always come up. It's totally normal. Let's walk through some of the most common ones I hear from business owners and get you some straight, practical answers you can use today.

This is probably the single most important concept for any owner to grasp. Think of it this way: profit is the story your books tell you at the end of the month. It's your revenue minus your expenses—an accounting number on a piece of paper. Cash flow is the reality in your bank account. It’s the actual cash moving in and out.

Here's a classic scenario: You could have a fantastic, profitable month on your income statement, but find yourself completely unable to make payroll. How? Because your clients haven't paid their invoices yet. You've earned the profit, but you don't have the cash. Cash is the fuel that keeps the engine running day-to-day. Profit is the destination. You need the fuel to get there.

For most small businesses, a weekly review is the perfect rhythm. It's frequent enough to catch little hiccups before they turn into big, scary problems. You’ll have enough time to actually do something about them.

But, if your business is something like a busy café or a retail shop with daily sales swings and tight margins, a quick daily check-in is a lifesaver. Regardless of your weekly habit, a deep-dive monthly review is non-negotiable. This is where you compare your forecast to what actually happened and get smart for the month ahead.

The point of checking in so often isn't about micromanaging every single dollar. It's about building a constant, clear-eyed awareness of where you stand. It allows you to make decisions from a place of confidence, not last-minute panic.

Okay, your forecast is flashing a warning sign. Don't panic. Take a breath, and then act with a two-pronged strategy: speed up what’s coming in and slow down what's going out.

This one-two punch is often all you need to create the breathing room to get through a tight spot.

They can be, but you have to see them for what they are: a tool, not a cure. A line of credit is brilliant for smoothing over predictable, temporary gaps. Think of a seasonal slowdown before the holiday rush or that period when you're waiting on a huge client payment.

But here’s the trap: using debt to paper over a fundamental flaw in your business is a disaster waiting to happen. If your pricing is wrong, your collection process is broken, or your spending is out of control, a loan is just a bandage on a wound that needs stitches. You'll just end up with the same problems, plus a debt payment. Fix the underlying issue in your cash cycle first. For a deeper look into building financial resilience, check out this great guide on Mastering Small Business Cash Flow.

At Jackpot Candles, we believe in creating moments of surprise and delight. Our premium soy candles and bath bombs offer a luxurious experience with an exciting jewelry reveal inside, turning a simple pleasure into a memorable event. Discover your surprise today!

Comments will be approved before showing up.